INVESTOR FACILITATION

A dedicated project committee screens investment projects to ensure that all project criteria are met and the project processes fall within the regulated environmental framework. Projects that meet the required criteria are channeled to the Board of Investment of Sri Lanka and other relevant government agencies for project approval.

Screening and approval of investment proposal is carried out in collaboration with the Board of Investment, which is the national agency tasked with promoting and facilitating foreign direct investment within Sri Lanka.

Investor Benefits

- Savings in time and cost of transportation due to easy access to port services for imports and exports.

- Warehousing facilities for bulk storage.

- Free Trade Agreements with India, Pakistan, Bangladesh and Singapore.

- GSP & GSP + with USA, Canada, Australia and Europe.

- Access to skilled labour.

- Complimenting and constantly expanding road networks and expressways within the island.

- Sufficient water and power capacity to accommodate investor’s project requirements.

- Public facilities such as hospitals and recreational activities.

One-Stop Service Center (OSS)

The One Stop service Centre at the Maritime Center of the Hambantota International Port consists of representatives from Board of Investment of Sri Lanka (BOI) and Sri Lanka Customs, who work in close collaboration with HIPG to facilitate the provision of all required services in a seamless manner.

Project screening flow

Key line agencies

Investment Policy and Incentives

The investment policy of Sri Lanka is geared towards realisation of sustainable development of the country taking into consideration its development priorities and comparative advantages and opportunities to ensure improvement of productivity and international competitiveness for export led economic growth to improve the quality of life of its people.

The key legislations applicable for facilitating investment in Sri Lanka are as follows

The BOI was established in 1978, as the National Investment Promotion Agency of the country and BOI law No 4 of 1978 and its amendments are the principal law applicable for granting approval for investment. The BOI is entrusted to promote and facilitate both local and foreign investment in Sri Lanka and functions as central facilitation point for investors. The BOI grants two kind of Investment approvals.

Investment approval under section 16 of BOI Law

- The investment approval under section 16 of BOI law are being granted for specific business activities subject to terms and conditions specified in the Foreign Exchange Act No 12 of 2017 among other things.

- These projects are not entitled for any tax or duty exemptions under BOI law.

- These projects are governed under the normal laws of the country.

- However, they are entitled for benefits available for such business activities under the normal laws of the country.

- Once the approval of the BOI is granted for investment, the investor is required to incorporate a company with the Registrar of Companies and commence the operations.

- Minimum Investment Requirement: US $ 250,000.

The terms and conditions set out in the Foreign exchange Act No 12 of 2017 with regard to entry of foreign investment and applicable for such projects approved under section 16 of BOI Law.

The terms and conditions applicable for such projects under Foreign Exchange Act No 12 of 2017 are explained in the appendix 3.

Approval under section 17 of the BOI Law

The BOI is also empowered to grant approval for investment with income tax and custom duty exemptions under section 17 of the BOI Law. These projects are treated as ‘Privileged Companies and the Investor is required to enter into an agreement with the BOI where terms and conditions applicable for such investment projects and its operations will be detailed. The principal benefits that are conferred to Investors under this agreement (depend on business activity) will include among other things;

- Exemption from payment of Income Tax.

- Exemption for payment of Custom duty on Import of Capital Goods and Raw Materials.

- Exemption from Exchange control restrictions.

- Exemption from Import control regulations.

However, with a view to harmonize the income tax incentives for projects operating outside the BOI Law, at present a set of incentives are available under the Inland revenue Law No 24 of 2017 for all the investors whether BOI or outside.

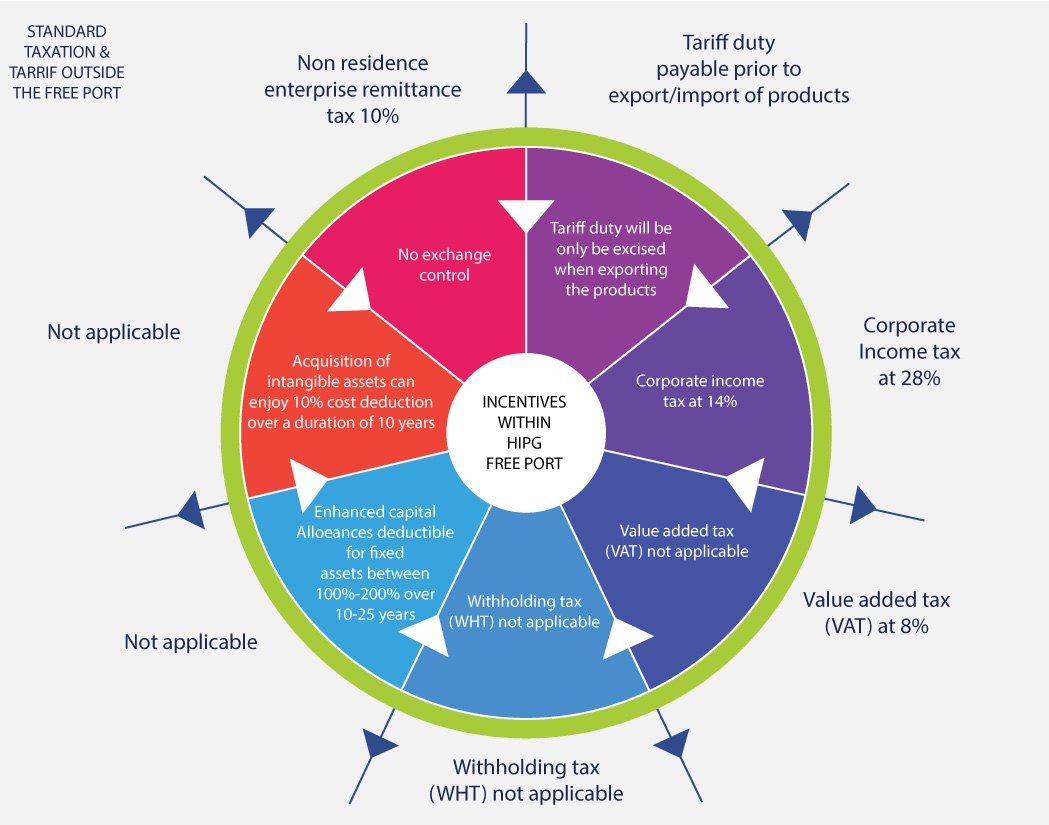

This legislation has simplified the taxation law in Sri Lanka while introducing a new incentive regime for investors. While maintaining the standard corporate income tax rate at 28%, this law provides for a reduced rate of 14% for specific sectors such as SMEs, Exports of Goods and Services, IT, Education, Tourism and Agriculture. Enhanced capital allowance has been offered to investors for their fixed capital investment over and above the normal depreciation.

This legislation was introduced to promote Sri Lanka as an emerging trading hub and facilitates related specific trading and services activities. Free Ports and Bonded Areas have been set up to create trade related infrastructure to facilitate Sri Lanka’s import and export of goods and services with freedom to carry out transactions in convertible foreign currency.

Foreign exchange controls have been greatly liberalized under the Foreign Exchange Act No.12 of 2017 and investors are allowed to directly deal with the banks for their transactions unless Central Bank approval is specifically needed. Free flow of transfers are allowed through Inward Investment Accounts and through Outward Investment Accounts within the given limits. This Foreign Exchange Act repeals the Exchange Control Act (Chapter 423).

Land Policy

Land (Restriction on Alienation) Act No.38 of 2014

A new land law was promulgated in 2014 which permitted lease of land for foreign investments and outright transfers will only be permitted when the foreign shareholding is less than 50%. The land lease period is subject to a maximum tenure of 99 years. The outright lease tax which was introduced in this Act has now been withdrawn and foreign investors are not liable to pay any lease tax when leasing a land. However, condominium properties can be purchased outright with no restrictions on nationality.

Summary of Investment Incentives

Following incentives are available for investors under Inland Revenue law at present.

| Location Depreciable | Expenses Incurred on Assets* | Enhanced Capital Allowance | Extended Period for Deducting Unrelieved Losses | Exemption from Dividend tax & Exemption of employment income from WHT |

|---|---|---|---|---|

| Nothern Province | US$ 3 M and < = US $ 1,000 M | 200% | 10 | N |

| US $ 1,000 M | 200% | 25 | Y | |

| Other than Northern Province | US $ 3 M and < = US $ 100 M | 100% | 10 | N |

| US 100M and > = US $ 1,000 M | 150% | 10 | N | |

| US $ 1,000 M | 150% | 25 | Y |

Intangible Assets (class 5)

Classification of Depreciable Assets

- Class 1 - Computers and data handling equipment together with peripheral devices.

- Class 2 - Buses and minibuses, goods vehicles; construction and earthmoving equipment, heavy general purpose or specialized trucks, trailers and trailer-mounted containers; plant and machinery used in manufacturing.

- Class 3 - Railroad cars, locomotives, and equipment; vessels, barges, tugs, and similar water transportation equipment; Aircraft; specialized public utility plant, equipment, and machinery; office furniture, fixtures, and equipment; any depreciable asset not included in another class.

- Class 4 - Buildings, structures and similar works of a permanent nature.

- Class 5 - Intangible assets, excluding goodwill – applicable only for normal depreciation.

Special Incentives for State Owned Company

| Category | Expenses Incurred on Assets or Shares | Enhanced Capital Allowance | Extended Period for Deducting Unrelieved Losses | Exemption from Dividend tax & Exemption of employment income from WHT |

|---|---|---|---|---|

| State Owned Company | US $ 250 M | 150% | 25 | Y |

“State owned company” means any company, where fifty per centum or more of the shares are held by the Government and includes a company of which forty per centum or more of the shares held by the Government are acquired by a person for an amount not less than USD 250 million.

Temporary Concessions

| Location | Expenses Incurred on Depreciable Assets* | Enhanced Capital Allowance |

|---|---|---|

| Northern Province | Up to US $ 3 M | 200% |

| Other than Northern Province | Up to US $ 3 M | 100% |

- Class 1: computers and data handling equipment together with peripheral devices and Class 4: buildings, structures and similar works of a permanent nature.

- Depreciable assets (other than intangible assets) comprising plant or machinery that are used to improve business processes or productivity and fixed to the business premises.

| Sector | Incentives | Period (after commencement of the Act) |

|---|---|---|

| Business of Life Insurance | Reduced CIT rate of 14% | 3 years |

Information Technology

|

Additional deduction equal to 35% (of the total amount deducted for the year under the IR Act that represents payments made by the company which are to be included in calculating the taxable income of its employees) | ceiling of 5 years |

| Headquarters Relocation (established on or after October 1, 2017 | CIT Rate at 0% | 3 years |

| Renewable Energy (Which entered into a Standardized Power Purchase Agreement on or before November 10, 2016 with the Ceylon Electricity Board) | Reduced CIT rate of 14% | 3 years |

| Research and Development | Additional deduction equal to 100% of the total amount of research and development expenses | 3 years |

Free Trade Agreements

The Indo-Sri Lanka Free Trade Agreement (ISFTA) signed on 28 December 1998 and entered into force with effect from 1 March 2000.

Since the end of March 2003, Sri Lanka has received total duty free access to the vast Indian market under the ISFTA for more than 4,200 products (HS Codes at 6 digit level).

Classification of Duty Concession Schedules under Indo - Lanka FTA

| Type of Duty Reduction | Sri Lanka's Commitment* | India's Commitment* |

|---|---|---|

| Negative List (No Concession List) | 1,220 | 198 |

| Tariff Rate Quota (TRQ) | 5 | |

| Tea | 235 | |

| Garments | 5 | |

| Vanaspathi, Bakery Shortening | 553 | |

| Margarine and Pepper | 4,004 | 4,228 |

| Margin of Preference (MOP) | 5,224 | 5,224 |

| Textiles | ||

| 100% Duty Free List (Zero Duty List) |

Rule of Origin (ROO)

- 35% Domestic Value Addition (DVA) (25% DVA if raw materials are imported from partner country)

- Change of Tariff Heading criteria at 4-digit level

- A sufficient process

The focal point and the authority for issuing Indo - Lanka FTA Certificates of Origin is the Department of Commerce, Sri Lanka and Federation of Chamber of Commerce.

Sri Lanka's second Free Trade Agreement (FTA) between Pakistan and Sri Lanka commenced on 12th June 2005. Since March 2009 Sri Lanka has duty free market access for more than 4,500 products. Sri Lanka has also completed all her phasing out commitments in November 2010.

Classification of Duty Concession Schedules under Pakistan - Sri Lanka FTA

| Type of Duty Reduction | Sri Lanka's Commitment* | India's Commitment* |

|---|---|---|

| Negative List (No Concession List) | 695 | 498 |

| Tariff Rate Quota (TRQ) | ||

| Basmati Rice and Potato | 2 | - |

| Garments | - | 21 |

| Tea | 04 | |

| Margin of Preference (MOP) | - | 05 |

| Cosmetics | - | 11 |

| Betel Leaves | - | 01 |

| 100% Duty Free List (Zero Duty List) |

Rule of Origin (ROO)

- 35% Domestic Value Addition (DVA) (25% DVA if raw materials are imported from partner country)

- Change of Tariff Heading criteria at 6-digit level

- A sufficient process

The focal point and the authority for issuing Pakistan - Sri Lanka FTA Certificates of Origin is the Department of Commerce in Sri Lanka.

The Free Trade Agreement (FTA) between Sri Lanka and Singapore was signed on 23rd January 2018. The Sri Lanka-Singapore FTA (SLSFTA) is a landmark agreement as it is the first comprehensive agreement for Sri Lanka that includes investments and services beyond trade in goods. The Singapore-Sri Lanka FTA is part of a broader strategy of looking “East” to renew the country's trade relationships in the process of diversifying its markets towards Asia and focus on plugging into ASEAN supply chains.

It is expected that the protection to be given under SLSFTA to investors and to their investments will result in substantial increase in FDI utilizing the provisions of this agreement.

Sri Lanka's strategic location provides great opportunities to enter into free trade and partnership agreements with several of Asia's trade powerhouses. Sri Lanka is pursuing a more proactive free trade agreement (FTA) strategy and negotiations are ongoing with China to establish a deeper economic arrangement with India to supplement the near two decade old FTA.

Visa Facilitation

Being the Investment Promotional Agency of the country, the Board of Investment (BOI) plays a vital role in facilitating companies to enhance the ease of doing business in Sri Lanka. As such, BOI recommends visas for Investors and skilled workers under identified categories to the issuing authorities, the Department of Immigration and Emigration under Ministry of Internal Affairs, Wayamba Development and Cultural Affairs.

The BOI recommends different types of visas for Investors, dependents and expatriate workers of BOI approved projects under Sec. 17 and Sec. 16 of the BOI Act.

Type of visa recommendations

- Entry Visa / Multiple Entry Business Visa

- Residence Visa / Special Residence Visa

- Extension of Residence Visa

- Temporary Visa (maximum 03 months only)

Investors and expatriate employees should arrive in Sri Lanka using Entry Visa or Business Visa and within one month from the date of arrival the Entry Visa should be converted to Residence Visa with the recommendation of the BOI.

If the applicant leaves the country within the Entry Visa period (One month), no provisions are available to convert the same Entry Visa to Residence Visa, unless a fresh Entry Visa application is submitted.

Temporary Visa will be recommended for contracted technical workers (expatriates) for a period of 3 months for specific assignments after evaluation of such activities.